Why Cyprus needs "an" electricity interconnector

"Energy islands" will be uncompetitive in a world of abundant cheap energy

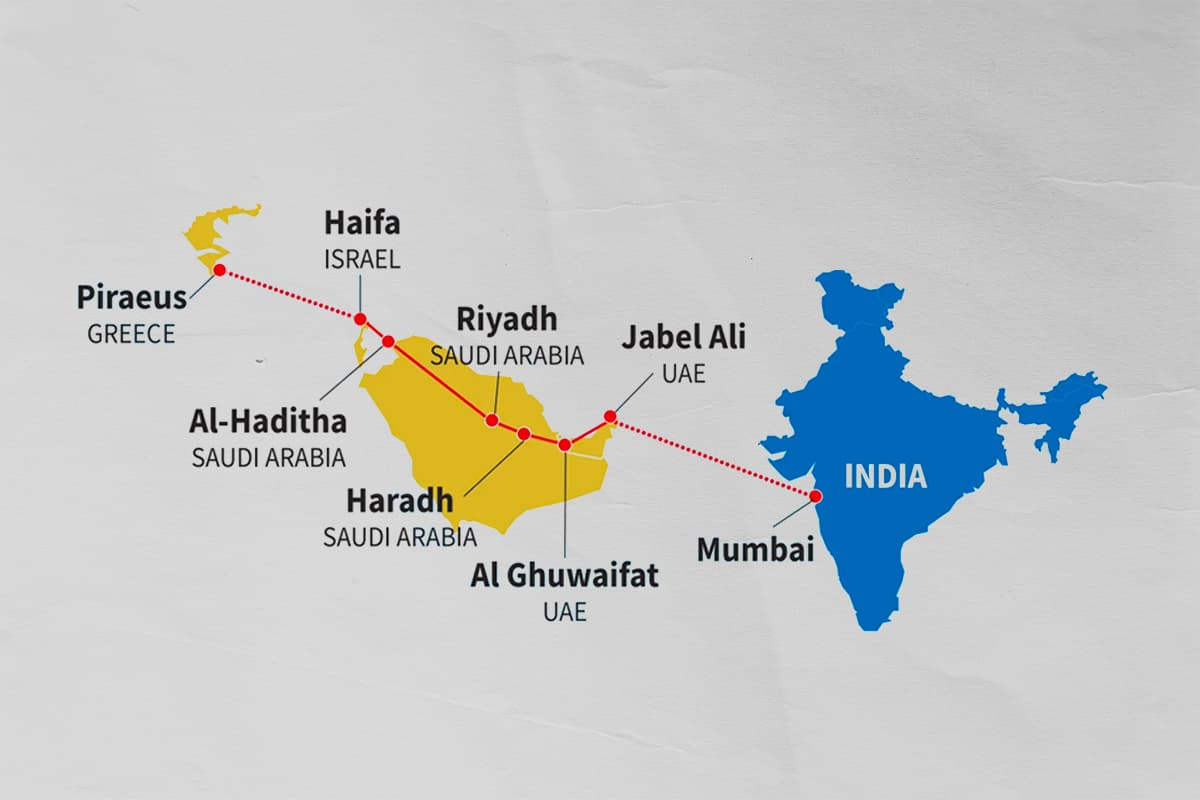

Illustration of the India-Middle East Energy Corridor (IMEC). Source IndianFoundation.in. Note that, in this illustration dated March 2025, neither Cyprus nor Turkey is invited!

Back in October 2019, energy specialist Nick Butler, former chair of the Cambridge Centre for Energy Studies and former special adviser to Gordon Brown when he was UK prime minister, visited Cyprus and gave a talk at the Economy Society.

What I remember most was him talking about the coming era of “abundant, cheap energy”. He showed slides predicting that wind and solar would account for more than 50% of all electricity generation in Europe by 2050, and that natural gas would account for a shrinking share. He showed figures of plans to send electricity cables across vast distances.

If you think that was all too long ago to be relevant, here is a more recent article by BioBased Press, talking in May 2025 of the era of the “SWB superpower” for solar, wind and batteries. One of the things it says you need in this SWP superpower era is “Electricity imports from neighbouring regions”. I’ll get onto that in a moment.

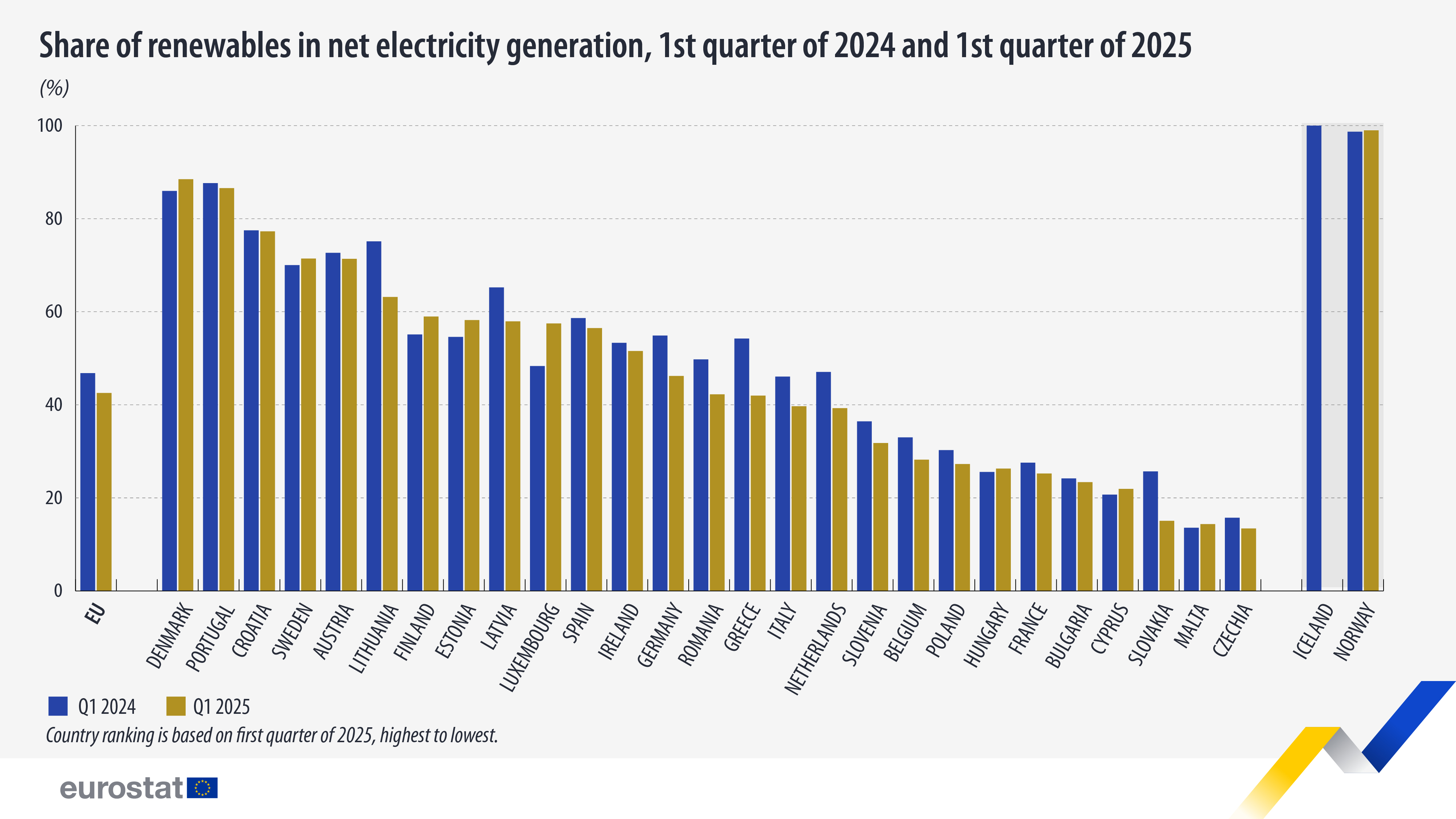

The natural gas share in electricity is shrinking

Figures from the European Commission show that we are getting to the “more than 50%” much earlier than 2050. In the first quarter of 2025 the share of renewables in “net” electricity generation in the EU was already as high as 42.5%.

Electricity production from natural gas, meanwhile, has been falling even before Russia’s full-scale invasion of Ukraine. Eurostat reports a preliminary 443,477 gigawatts (GW) of electricity production from natural gas in 2024, compared with 569,299 GW in the pre-pandemic year of 2019.

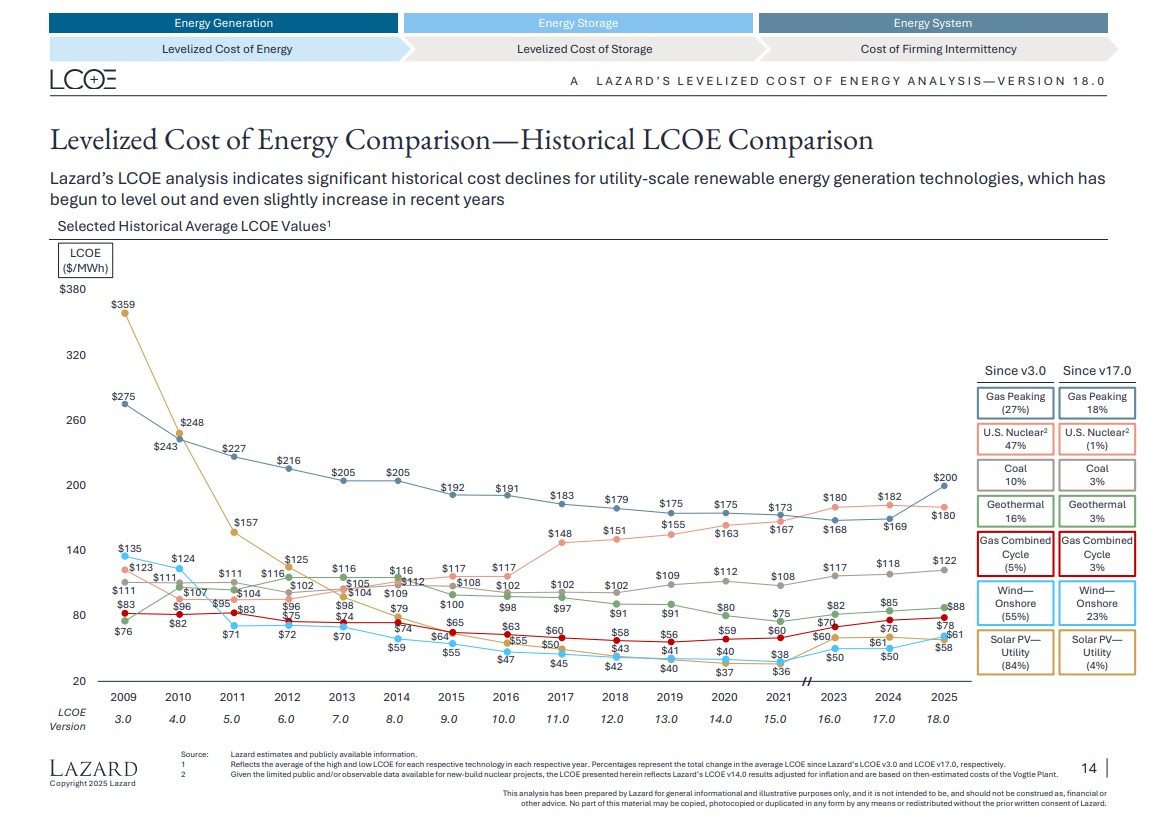

Wind and solar have been the cheapest sources since 2015

The key reason why gas was falling even in 2019 was cost. Every year the investment house Lazard produces the “levelized cost of energy” (LCOE) for different fuels, including renewables. And every year, renewables are cheaper, even without subsidies, than other sources. Below is a chart from the latest report for 2025. You can see that the LCOE of unsubsidized utility-scale photovoltaics and wind have been the cheapest fuel sources for about a decade.

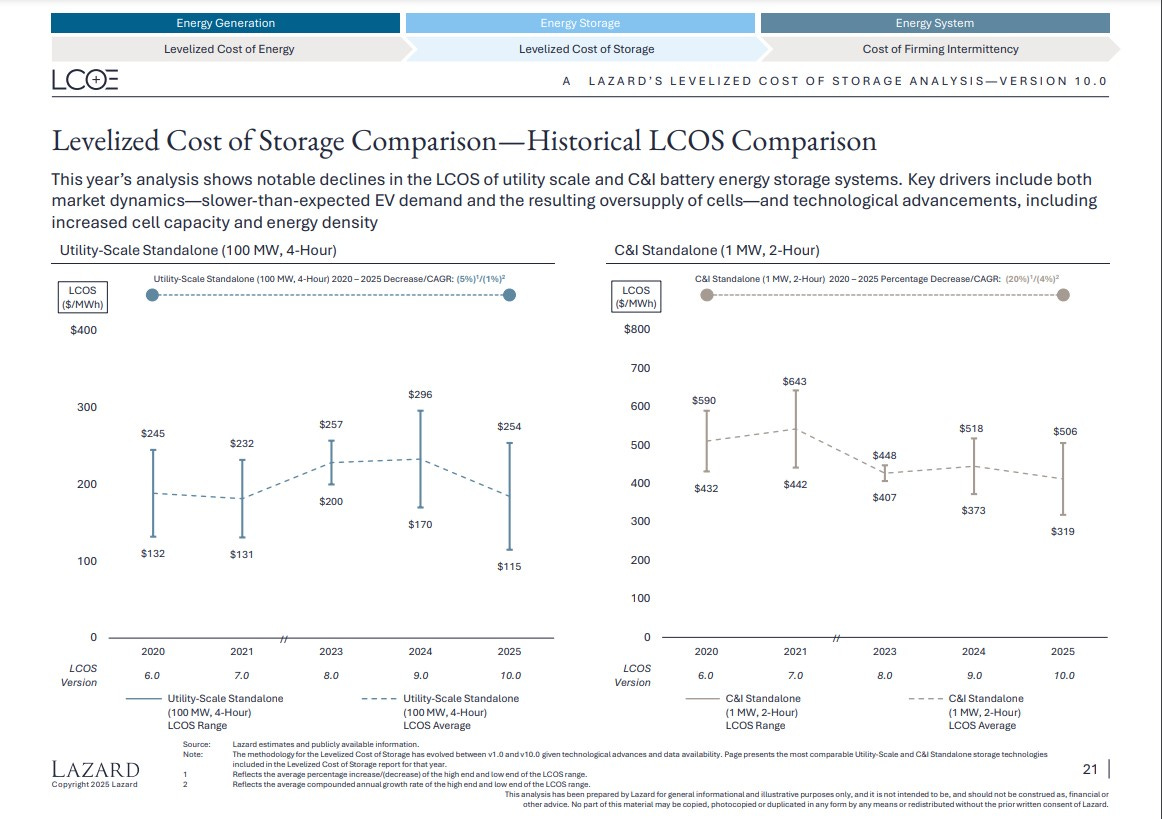

Once upon a time, you could protest at this statement and say, “but, cost of storage!” Well, it turns out that this is falling in price too.

Meanwhile uncertainty reigns in Cyprus

Here in wee Cyprus, however, we have got ourselves into a bit of a bind. For various reasons explained in this article I wrote in April, we are still stuck, in the year 2025, with the risk of blackouts this summer. Worse still, we need more electricity than ever for energy-hungry desalination plants because of a water crisis.

We have plenty of renewable energy sources (RES). But we do not know when the grid will have enough storage or the modern infrastructure to stop rejecting electricity produced from RES. New delays mean we still do not know when the terminal for importing (at least cleaner) liquefied natural gas (LNG) will be finished. This means that we do not know when the Electricity Authority of Cyprus (EAC) and the private Power Energy Cyprus (PEC) under construction can start producing electricity from natural gas.

For this reason we are still burning really dirty diesel and mazut (heavy fuel oil) for around 75% of electricity supply. Burning dirty fuels means we are still paying around €400m per year in emissions penalties.

Resistance to the Great Sea Interconnector

You would think, under these circumstances, that everyone in government and beyond would be fully behind the plan to end Cyprus’ energy isolation and link the electricity network to the rest of Europe via the Great Sea Interconnector (GSI): the project to send electricity from Greece’s Crete to Cyprus and eventually to Israel.

An interconnector would end the ever-present risk of blackouts. It would mean that there would be plenty of electricity for more desalination plants, more tourists and the energy-intensive data centres that are said to be looking at Cyprus but which would not come if we cannot keep the lights on. As Cyprus has the best solar profile in Europe, an interconnector should also open up the possibility of electricity exports to Europe.

{kind=link}

Alas, this is not the case. On the one hand, the energy minister, George Papanastasiou, is clearly pushing for the GSI and for the EU to put pressure on Turkey not to prevent the laying of cables. The Republic of Cyprus president, Nikos Christodoulides, also indicated support for the project at the beginning of the month.

On the other hand, it is clear that people in government, rumoured to be in the finance ministry, are against it. Indeed, the finance ministry blocked payments for the interconnector just this week. An article in Kathimerini this month quoted an anonymous source talking about “pouring money into a black hole”. This has been a persistent pattern for months. The energy minister says something positive about the interconnector; an anonymous source briefs against him.

Let’s see the naysayers’ figures

If the finance ministry is indeed against the project, it should come clean and show us its calculations. (New estimates have been submitted by Greece’s Independent Power Transmission Operator (IPTO or ADMIE), the GSI operator.) I trust the naysayers’ calculations would include the current cost of emissions while we wait for natural gas and home-grown RES to come on-stream. I trust they will include the lost investment from big US data centres because Cyprus cannot guarantee to keep the lights on. I trust that they would include the cost to the economy of being totally uncompetitive when it remains the only energy island in the world in the abovementioned age of abundant, cheap energy.

If the finance ministry’s private calculations do not include any of these considerations, then we should have a long, hard think about taking them seriously.

The ties that bind

Some of the resistance to the GSI comes from the behaviour of the Greek operator. Certainly the media in Cyprus are being briefed to believe that ADMIE/IPTO is trying to move the goalposts on an agreement that gave some certainty to the Cyprus government over costs.

Nevertheless, even when the uncertainty was apparently removed last September, the media briefings against the GSI continued. I think this is because there are two other reasons for resistance to the interconnector regardless of the cost.

The first is fear of competition from the GSI. A few years ago our biggest bank took a big bet on one of our biggest property developers, and decided to lend it €120m to build a gas-fired power plant. It did this without knowing for sure when the gas was coming. (Shameless plug: maybe the bank or the borrower should have had me as an energy consultant, or at least been buying my monthly reports.)

These days, the bank’s entire non-performing exposures (NPEs) amount to only €190m. If that loan were to go sour, it would lead to a 63 percentage-point increase in the bank’s NPE ratio (other things being equal). Alternatively, the borrower might have to dip into its (likely) more profitable property arm to pay the debt.

In short, the ideal scenario for the bank and borrower are that the new gas-fired plant is up and running before any interconnector comes. That way, any surplus from gas or renewables produced in Cyprus can be exported. The gas imports are likely to come long before the interconnector is completed in any case. But you can see why some people might want to delay the GSI, or completely prevent it from being built if they believe that there will be no surplus to export.

A second potential reason is that people have decided that we should now hook up with the India-Middle East Energy Corridor (IMEC) instead. This is a project that would link India, Saudi Arabia, Israel and Greece with electricity cables, data cables and so on. As someone explained to me, the IMEC concept is a corridor, so does not necessarily exclude the GSI. However, the behaviour of some in Cyprus, plus briefings to the media, seem to suggest that people think that yes to IMEC means no to the GSI.

Personally, I don’t care where the interconnector comes from or goes to. Let’s just have one, or ideally as many as possible to protect from the new geopolitical risk called cable-cutters. But if you are thinking of throwing money at IMEC, do pay attention to the following two factors.

First, everyone knows IMEC cannot not get started until Saudi Arabia and Israel are on better terms. And everyone knows this means, at the very least, a ceasefire in Gaza and possibly a whole bunch of credible promises about a path to Palestinian statehood that will not be easy to get.

Second, the current plan for IMEC, as you can see from the first image, does not include Cyprus. Nor, importantly, does it include Turkey. If Turkey is not included in a grand plan to connect the Middle East and Israel through electricity cables, it will do what it always does when it is being left out. It will wade in and trash everything. To sanitize a phrase, it is better to have them peeing out than peeing in.

So what is the best energy strategy?

So what is the best strategy for electricity under these circumstances?

If Cyprus is to have a competitive economy in the era of cheap energy, it needs to get in on the cheap energy game as fast as possible. Right now the best way of doing that is through continued investment in storage and continued investment in the GSI, as it is more mature than the IMEC.

That might mean finding artful ways to appease important stakeholders who might have taken a bet on the wrong horse. It might mean relying on Greece to work behind the scenes to find an interconnector solution that somehow includes Turkey and the Turkish Cypriots.

At least an interconnector that would include Turkey would be a confidence-building measure (CBM) worth lobbying for, as interconnectivity would have clear benefits for everyone on the island. No more blackouts; no more filthy smoke billowing out from power stations in the north and the south and filling the lungs of the island’s children. Cheaper electricity for all and the opportunity to earning revenue from exporting it. It’s a no-brainer.

If you want my premium monthly in-depth product, check out Sapienta Country Analysis Cyprus and other deep-dive reports here. And if you can’t afford that but want the executive summary only for just €100/year*, you can find that here on Substack, at Cyprus Pocket Brief.

Or keep these articles and hugely labour-intensive videos coming by supporting this publication, Sapienta Cyprus Snippets, for just €49 per year.*

*Monthly payments are a massive administrative headache, so since I can’t switch them off I have effectively banned them by setting the monthly price the same as the annual.